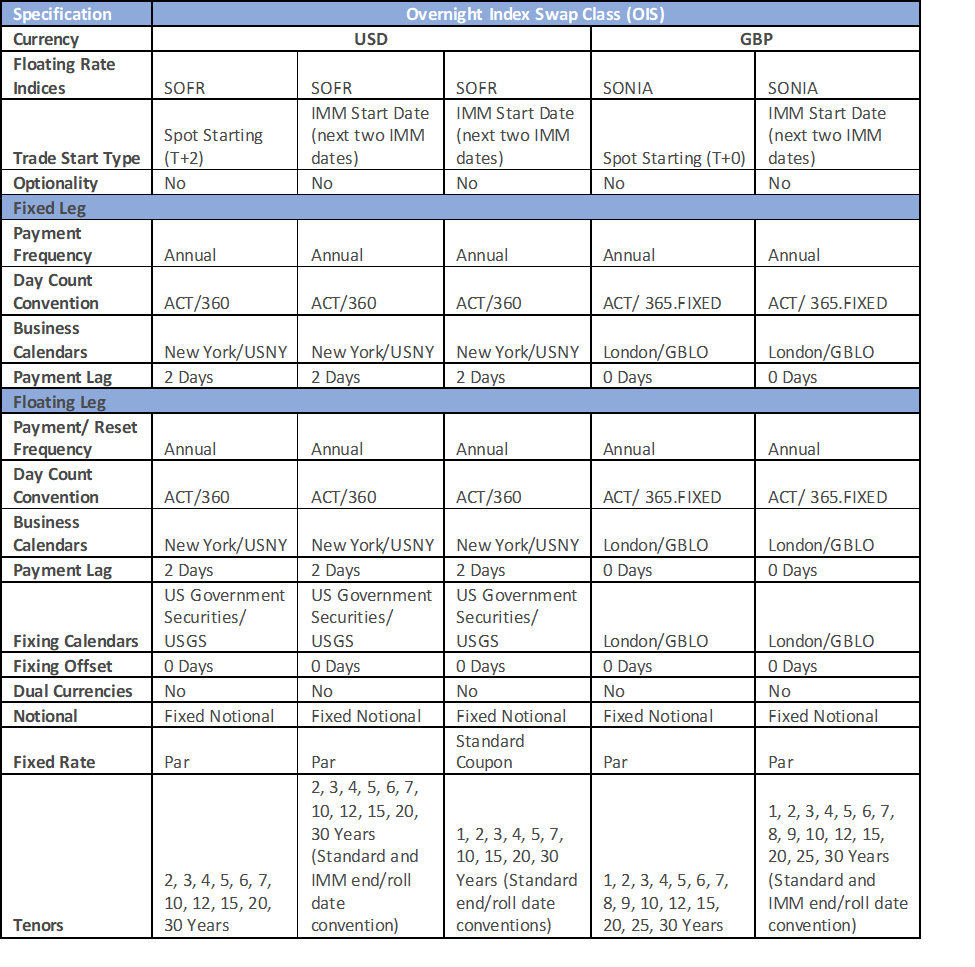

USD & GBP SOFR/SONIA SWAPS

The terms and conditions of the swap as established by the DCO in its rules or bylaws are incorporated by reference herein and are the terms and conditions of the swap. The swaps have the following characteristics:

| Currency: | U.S. Dollar |

| Floating Rate Indexes: | LIBOR/LIBOR LIBOR/Fed Funds LIBOR/OIS Including Spread over Treasuries LIBOR/MXN-TIIE-Banxico (MXN IRS Benchmark) LIBOR/ICP (CLP IRS Benchmark) |

| Stated Termination Date Range: | 28 days to 50 years Spot & Forward starting, and broken dates (bespoke tenors) |

| Optionality: | No |

| Dual Currencies: | No |

| Conditional Notional Amounts: | No |

| Currency: | U.S. Dollar (USD) |

| Floating Rate Indexes: | LIBOR |

| Stated Start Date Range: | 28 days to 50 years Spot & Forward starting, and broken dates (bespoke tenors) |

| Optionality: | No |

| Dual Currencies: | No |

| Conditional Notional Amounts: | No |

| Currency: | U.S. Dollar |

| Floating Rate Indexes: | LIBOR |

| Stated Termination Date Range: | 3 days to 3 years |

| Optionality: | No |

| Dual Currencies: | No |

| Conditional Notional Amounts: | No |

| Currency: | U.S.Dollar |

| Fixed Coupon: |

http://www.sifma.org/services/standard-forms-and-documentation/swaps/ |

| Floating Rate Indexes: | LIBOR |

| Tenors: | 1y, 2yrs, 3yrs, 5yrs, 7yrs, 10yrs, 15 yrs, 20 yrs, 30yrs |

| Effective Dates: | IMM dates (3rd Weds of March, June, September, December) |

| Currency: | U.S. Dollar (USD) (“OIS”) |

| Floating Rate Indexes: | LIBOR |

| Stated Termination Date Range: | 7 days to 50 years Spot & Forward starting, and broken dates (bespoke tenors) |

| Optionality: | No |

| Dual Currencies: | No |

| Conditional Notional Amounts: | No |

Recent Comments